The Japan Real Estate Investment Guide

An institutional roadmap for navigating the Japanese acquisition process, tax structures, and risk mitigation.

The Macro Thesis

The "Yield Gap" & Positive Carry

Japan remains a global outlier where property yields (Cap Rates) sit significantly above the cost of debt. While central banks globally have hiked rates, the Bank of Japan’s gradual normalization ensures that a Positive Carry remains the primary driver for international capital.

Key Performance Indicators

The Institutional Spread: In Tokyo, prime residential and office assets typically yield 4.0% – 5.5%, while senior debt can be secured at 1.2% – 1.9%.

Cash-on-Cash Enhancement: This spread allows investors to utilize low-cost local financing to amplify equity returns, often achieving double-digit returns on high-quality assets.

Market Resilience: Unlike markets where financing exceeds yields (negative carry), Japan’s structure provides a significant “cushion” against moderate interest rate fluctuations.

Yield Spread Analysis: The Positive Carry Advantage

While global interest rates have inverted, Japan maintains a +250 to +560 bps spread, providing unique leverage efficiency for institutional capital.

Security, Sovereignty, and The Yen

An overview into the regulatory and macroeconomic moats that protect international investors in the Japanese market.

Strategic Currency Entry

The current Yen valuation provides a unique entry point for USD/EUR-based capital. Investing in hard assets allows for dual-revenue potential: property appreciation and long-term currency recovery.

Unrestricted Foreign Ownership

Unlike many neighboring Asian markets, Japan allows 100% freehold land ownership for foreign entities. There are no "Foreign Buyer" surcharges or special restrictions on title acquisition.

Safe Haven Fundamentals

Japan offers a highly transparent legal framework and a "Rule of Law" environment. Political stability and predictable tax structures make it the G7's primary destination for capital preservation.

The Tokyo Magnet: Strategic Urban Migration

Countering national demographic trends through concentrated urban growth and structural demand in Japan’s core metropolitan hubs.

Concentrated Demand: While Japan’s rural populations consolidate, the Greater Tokyo Area continues to attract young professionals and international talent, creating a “virtuous cycle” of demand for modern residential and office space.

Occupancy Resilience: Institutional-grade assets in Tokyo and Osaka historically maintain occupancy rates above 95%, even during periods of global economic cooling.

The “Megacity” Premium: Investment is focused on the “Kanto” and “Kansai” regions, where infrastructure density and economic output rival entire G7 nations, providing a massive “moat” for property values.

95%+ Occupancy

Asset Class Intelligence

- En-bloc Residential (Multi-family)

- Commercial & Office

- Hospitality (Hotels & Ryokan)

The primary target for defensive capital and stable, long-term yield.

Investment Thesis: Focus on “Needs-Based” real estate. By owning entire apartment buildings in high-density urban corridors, investors benefit from high liquidity and ultra-stable occupancy rates that are decoupled from economic cycles.

Yield Benchmarks:

Tokyo (23 Wards): 4.0% – 5.0%.

Regional Hubs (Osaka/Nagoya): 4.8% – 5.8%.

Key B2B Metric: Unit Mix: Institutional buyers prioritize a mix of 1K/1LDK (targeting the growing single-person household demographic) and 2LDK (small families) to ensure a diversified tenant base.

The “KisoBase” Advantage: Our directory focuses on Shin-Taishin (post-1981) assets, ensuring that your residential portfolio meets the strict seismic and bank-financing requirements of top-tier Japanese lenders.

Strategic positioning in high-demand business districts with a focus on tenant “stickiness.”

- Investment Thesis: While the “Remote Work” narrative persists, Tokyo’s office culture remains resilient. Boutique offices in prime districts (Minato, Chuo, Shibuya) are outperforming the market due to their appeal to the growing tech and startup sectors.

- Yield Benchmarks:

Grade-A (Central Tokyo): 3.2% – 4.2%.

Grade-B / Boutique: 4.0% – 5.2%.

- Institutional Metrics: WALE & Efficiency:

- WALE (Weighted Average Lease Expiry): Investors look for a WALE of 3.5+ years to ensure revenue predictability and minimize immediate leasing risk.

- Efficiency Ratio: Modern boutique offices strive for an 80%+ ratio (Net Lettable Area vs. Gross Floor Area), maximizing the income-generating potential of every square meter.

- The “KisoBase” Advantage: We vet commercial listings for BCP (Business Continuity Planning) features, such as dual-grid power and high seismic damping, which are mandatory for attracting top-tier corporate tenants.

High-yield operational assets capturing Japan’s unprecedented global tourism surge.

- Investment Thesis: Hospitality is a “Daily Mark-to-Market” business. Unlike office or residential rent, hotel room rates (ADR) can be adjusted in real-time to track inflation and demand, making this the ultimate hedge in a normalizing interest rate environment.

- Yield Benchmarks:

- Business/Limited Service Hotels: 5.5% – 7.5%.

- Luxury Hotels & Ryokans: 6.5% – 9.0%+ (Value-add).

- Institutional Metrics: RevPAR & ADR:

- RevPAR (Revenue Per Available Room): The primary KPI. Post-2024, Tokyo and Kyoto have seen RevPAR levels exceed pre-pandemic peaks by 25%+, driven by record-high Average Daily Rates (ADR).

- GOP Margin: Investors analyze the Gross Operating Profit to ensure the operator is managing high labor and utility costs effectively.

- The “KisoBase” Advantage: We specifically identify assets with Operator Flexibility, allowing buyers to bring in their own management brands or optimize existing operations to “force” yield appreciation.

The Institutional Acquisition Framework

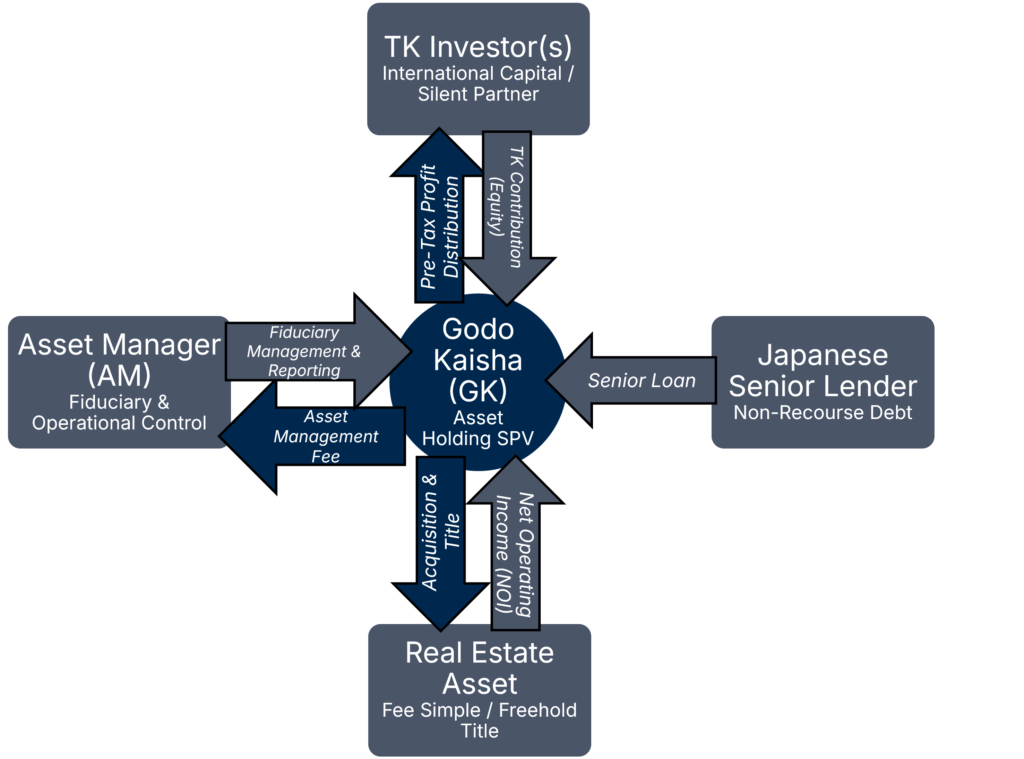

Tax-Efficient Investment Vehicles (GK-TK)

In Japan, sophisticated investors rarely buy property directly in their own name. Instead, they use a “de-linked” structure to optimize tax and liability.

The GK (Godo Kaisha): A Japanese limited liability company that acts as the Special Purpose Vehicle (SPV) to hold the asset.

The TK (Tokumei Kumiai): A “Silent Partnership” agreement. Investors provide capital to the GK in exchange for a share of the profits.

The B2B Benefit: Under this structure, profits are distributed to investors before corporate income tax is applied at the GK level, effectively avoiding double taxation.

The GK-TK Flowchart: Structural Optimization

A visual guide to the standard 'Silent Partnership' structure used for tax-efficient Japanese real estate acquisitions.

The Seismic Standard: Shin-Taishin

Japan’s Building Standard Act was overhauled on June 1, 1981. For an institutional investor, this date is the “Gold Standard” for risk mitigation.

Shin-Taishin (Post-1981): Buildings designed to resist major earthquakes without collapsing. These assets are highly bankable and easier to insure.

Kyu-Taishin (Pre-1981): Older structures that may require expensive seismic retrofitting. While they offer higher “headline” yields, they often fail institutional due diligence and are difficult to finance.

KisoBase Protocol: We prioritize Shin-Taishin assets to ensure your capital is protected by modern engineering standards.

Seismic Risk & Structural Compliance

A technical comparison of Japan’s Building Standard Act (BSL) eras and their impact on institutional bankability.

| Feature | Kyu-Taishin (Pre-1981) | Shin-Taishin (Post-1981) |

|---|---|---|

|

Regulation Date |

Buildings permitted before June 1, 1981 |

Buildings permitted after June 1, 1981 |

|

Design Logic |

Designed to resist “medium” earthquakes (Shindo 5) |

Designed to resist “major” earthquakes (Shindo 6-7) |

|

Institutional Status |

Generally considered “Non-Core” / Risky |

Gold Standard for institutional portfolios |

|

Bankability |

Limited; most major banks require seismic retrofitting |

High; standard for senior debt and non-recourse loans |

|

Insurance Cost |

Higher premiums; often excludes full earthquake coverage |

Standard rates; fully insurable for earthquake damage |

|

Resale Value |

Significant “liquidity discount” due to financing hurdles |

Maintains premium value; high liquidity among REITs |

Land Title: Freehold vs. Leasehold

Understanding the “bundle of rights” is critical for long-term valuation.

Freehold (Owenship): You own both the building and the land beneath it. This is the preferred status for 99% of international B2B investors.

Leasehold (借地権 – Shakuchiken): You own the building, but pay rent for the land. While the entry price is lower, these assets can be harder to exit as the lease term nears expiry.

| Feature | Freehold (Shoyuken) | Leasehold (Shakuchiken) |

|---|---|---|

|

Ownership Scope |

You own both the land and the building. |

You own the building; the land is leased. |

|

Asset Longevity |

Indefinite ownership; no expiry. |

Typically 20–30 years; subject to renewal. |

|

Monthly Costs |

Fixed Property Taxes only. |

Property Taxes + Monthly Land Rent (Chidai). |

|

Bankability |

High. Standard for all major lenders. |

Limited. Many banks reduce the LTV significantly. |

|

Exit Strategy |

High liquidity; preferred by J-REITs. |

Restricted; requires landowner consent for sale. |

|

CapEx Impact |

None on land; full control over rebuild. |

Rebuilding often requires a “Reconstruction Fee.” |

B2B Tip: Always verify the ‘Boundary Survey’ (Sokuryo). In Japan, an asset without a finalized boundary survey can lead to significant delays during the resale process.

Strategic Exit Horizon & Value Optimization

A structured 5-to-7 year roadmap designed to stabilize operations and compress exit yields for institutional disposition.

Acquisition & Integration

Closing the GK-TK structure, securing Senior Debt, and onboarding the Asset Manager.

Operational Alpha

Implementation of CapEx (renovations) and optimizing Gross Operating Profit (GOP) through professional management.

Performance Stabilization

Reaching target occupancy (>95%) and establishing a consistent track record of Net Operating Income (NOI).

Disposition & Liquidity

Marketing the stabilized asset to the Japanese secondary market (J-REITs, Pension Funds) to realize capital gains.

Institutional Liquidity & Secondary Market Depth

Japan’s mature real estate ecosystem ensures multiple exit channels for stabilized, institutional-grade assets.

| Buyer Type | Primary Motivation | Preferred Asset Class |

|---|---|---|

|

J-REITs |

Dividend yield stability and portfolio growth. |

Residential, Grade-A Office, Logistics. |

|

Pension Funds |

Ultra-long-term capital preservation. |

Core Residential & Central Office. |

|

Foreign PE Funds |

Portfolio aggregation for large-scale exits. |

Mixed Portfolios & Hospitality. |

|

Local Strategics |

Operational control and brand expansion. |

Hotels, Ryokans, and Retail. |

Institutional Due Diligence Checklist

A practical framework for evaluating asset quality and structural compliance within the Japanese market.

Structural & Legal

-

Seismic Status

Verify "Shin-Taishin" (Post-1981) permit dates to ensure building safety and financing eligibility.

-

Title Verification

Confirm 100% Freehold (Shoyuken) status and check for any undisclosed easements.

-

Boundary Survey

Ensure a finalized Sokuryo is present to prevent future legal disputes with neighbors.

Operational Performance

-

Rent Roll Audit

Analyze lease expiry profiles to identify near-term vacancy risks.

-

Efficiency Ratio

For office assets, verify the ratio of Net Lettable Area (NLA) to ensure yield optimization.

-

Historical Occupancy

Review 3-year trailing occupancy data to confirm market resilience.

Financial & Exit

-

GK-TK Optimization

Verify that the SPV structure allows for tax-deductible profit distributions.

-

PML Score

Request the Probable Maximum Loss report; a score under 15% is typically required for senior debt.

-

Exit Liquidity

Identify at least two viable J-REIT or private fund "exit channels" for the asset type.